Closing the Books: Basics & 8 Steps Guide

“The books” are a business’s revenue, expense, and income summary reports. Business owners can close their books by zeroing out their income and expense accounts and then plugging net profit (or loss) into the balance sheet.

Some accounting software automatically closes your income and expense accounts at year-end before adding your net profit (or loss) to your retained earnings account. Accounting software may create an automatic closing date as well as a password so transactions from before the closing date can’t be changed.

Key Takeaways

- Closing your books at the end of the year lets you know what your net profit or loss has been

- Accounting software can make keeping track of profits and losses much easier, especially as your business grows

- It may be prudent to close the books on a monthly basis rather than waiting until the year is over

- Financial statements can be generated once you have balanced your debits and credits.

- Closing your books regularly (monthly, quarterly, or annually) will prevent unwanted changes to your accounting data after generating financial reports, like an income statement

In this article, we’ll cover the following steps:

- Why Close the Books?

- How to Close the Books?

- 8 Steps to Close the Books

- Conclusion

- Frequently Asked Questions

Why Close the Books?

Regularly closing your books will prevent unwanted changes from occurring to your accounting data after you generate important financial reports for your accountant or tax professional. In accounting, it is important to ensure the expenses are recorded in the correct period, and closing books is a way to ensure no entries would be mistakenly recorded in incorrect periods so that the statements accurately reflect the actual income and expenses of each period.

How to Close the Books?

Closing your books is as simple as gathering the appropriate financial data within a specified timeframe, entering appropriate journal entries and financial information into the general ledger, and summing all ledger accounts. Before creating your final report, generate a trial balance, and if things are not adding up, check your work and enter adjusting entries until you are ready to create the final financial statement.

Your accountant often does these steps or uses professional accounting software to reduce errors. Click here to get started with FreshBooks accounting software.

8 Steps to Close the Books

Even if you ask your accountant to close your books for you, it’s important to understand the basic steps involved so you know what to expect. Below are the 8 steps you need to know.

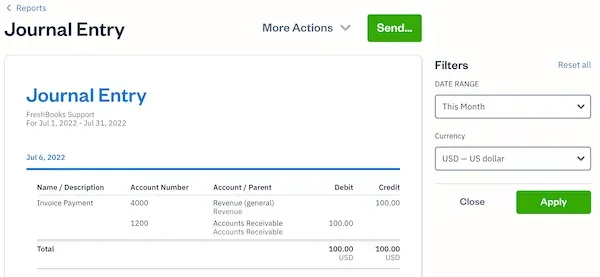

1. Transfer Journal Entries to the General Ledger

The journal is the first point of entry for all transactions. Journal entries are transferred to the general ledger when they’re posted to an account, such as accounts receivable.

Journal entries are easier to keep track of when organized. Free accounting templates can help you keep your journal entries in order and manage your bookkeeping in a straightforward manner.

Post the account totals from your cash payments and your sales and cash receipts journal to the appropriate general ledger account to close the books. Cash payments (“cash disbursements”) include any payments made by cash, check, or electronic fund transfer. The same is true of your cash receipts journal, though this journal tracks the inflow, not the outflow, of funds.

Most small companies close their books monthly, though some only do so at year’s end. That means you need to choose what entries you want to include. For example, you could choose all entries in 2025, or it could be for the month of January 2025 only.

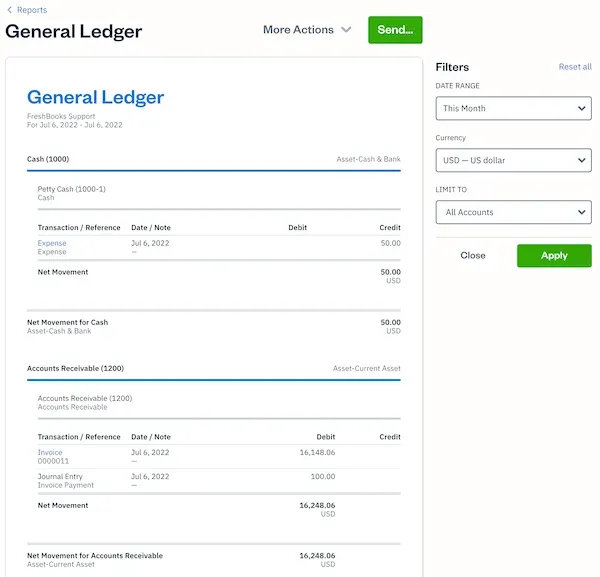

2. Sum the General Ledger Accounts

Add up all the transactions in each general ledger account. For example, add up all entries in accounts receivable. This gives you a preliminary ending balance for each account.

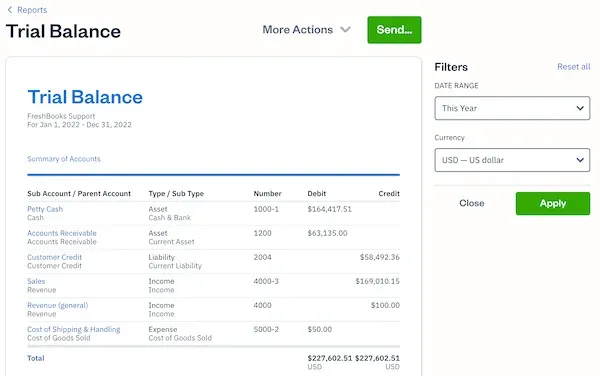

3. Make a Preliminary Trial Balance

Sum up the preliminary ending balances from the last step to make a trial balance. A trial balance is a report that adds up all the credits and debits in your business. You want your total credits to be the same number as your total debits—if they aren’t, go back and check your work. If the credits and debits are equal, your accounts balance, and you’re ready to go to the next step.

4. Enter Adjusting Journal Entries

Adjusting entries record items that aren’t noted in daily transactions. These items include accumulation (known as “accrual” in accounting) of real estate taxes or depreciation accrual, which need to be recorded to close the books. Adjusting items are made in the general journal.

It’s easier to make adjustments to journal entries when you use accounting software with connections to expert bookkeepers and tax prep services.

5. Make an Adjusted Trial Balance

Sum your general ledger accounts again to take into account the adjusted entries from the last step, and then add them all together to make a new trial balance, making sure your debits and credits are again equal. If they aren’t the same, go back and check your work.

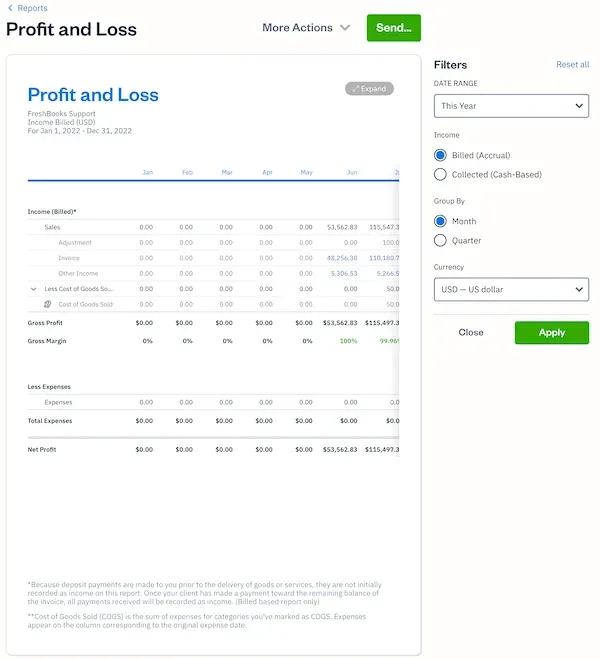

6. Generate Financial Statements

If the total debits and credits in your trial balance are the same, you’re ready to produce a balance sheet and income statement (also known as a “profit and loss report” or “P&L”). These reports can be generated automatically in your accounting software. They offer an overview of a business’s financial position at the end of the applicable accounting period, whether that’s the previous month or year. To ensure accuracy, it’s important to follow the correct format you can refer to our detailed guide Financial Statement Format to help you with this process.

7. Enter Closing Entries

For each fiscal year-end, closing the books also involves one more step, zeroing out your revenue and expense accounts by using journal entries, also called “closing entries.” Closing entries transfer profit and loss into the retained earnings account.

8. Generate a Final Trial Balance

The trial balance report will have balance sheet accounts as well as revenue and expense accounts. And all the account balances should be net zero. If they do, your general ledger account balances are correct and you’re all set for the next accounting period!

Businesses often use professional bookkeeping services to ensure they are on track financially, are tax-season ready, and are able to continue to grow and thrive. Get started here if you want to speak to a professional about your business cash flow.

Conclusion

Keeping your books balanced entails keeping a detailed record of all debits and all credits to each account. These records are then used to generate reports that can tell a business owner the financial status of their enterprise. This process helps owners stay on track with business goals and prepare for filing their income tax returns.

By closing your books on a regular basis (monthly, quarterly, or annually), a business owner can ensure the statements from the previous reports do not affect the current terms, which could produce an inaccurate report on the state of your business accounts.

FAQs on Closing the Books

What Does It Mean to Close the Books?

“The books” are a company’s record of financial transactions. The records are used to generate reports that tell an owner how much money flows in and out of their business.

Closing your books means that these reports are finalized. These finalized reports show a business’s financial position over a certain accounting period—whether a month or an entire year.

What Is the Purpose of the Closing Process?

The purpose of the closing process for each period is to avoid incorrectly recording income or expenses in previous periods. But closing the books for the financial year is more important for reflecting the correct retained earnings numbers on the balance sheet, which allows the start of a fresh financial year for profit and loss reporting.

What Accounts Are Affected by Closing Entries?

The following accounts are affected by closing entries:

- Revenue accounts

- Expense accounts

- Equity account – Retained Earnings

These temporary or “nominal” accounts are zeroed out and reset when closing entries are added to an accounting system so they don’t affect the next accounting period.

What Does It Mean To Close The Books Monthly?

When you close the books monthly, that means you make journal entries to ensure all transactions for the month have been captured. This makes it easier to do monthly tasks like bank reconciliation, sending sales tax reports to the state, paying your suppliers, and generating customer statements.

What Happens After Closing The Books In Accounting?

When you close your books at year-end, the accounts aren’t erased; instead, their balances are transferred to a permanent retained earnings account. Occasionally, revenue and expenses are transferred to an intermediate account called an income summary. Dividends are always transferred directly to retained earnings.

RELATED ARTICLES

When Should I Hire an Accountant

When Should I Hire an Accountant How To Choose an Accountant: 8 Things To Look For

How To Choose an Accountant: 8 Things To Look For What Is the Difference Between Bookkeeping and Accounting?

What Is the Difference Between Bookkeeping and Accounting? Keep Track of Expenses and Profits: A How-To Guide

Keep Track of Expenses and Profits: A How-To Guide How To Forecast Financial Statements: Balance Sheets, Income Statements

How To Forecast Financial Statements: Balance Sheets, Income Statements Why Are Financial Statements Important?

Why Are Financial Statements Important?