Accounting For Startups: Everything You Need To Know In 2025

Accounting for startups involves keeping accurate records of financial transactions and examining your finances to identify opportunities for growth and improvement.

Startups need to build a solid accounting foundation to stay organized, increase efficiency, obtain financing, control expenses and identify possible risks and opportunities for the business. Whether you hire an accountant or opt for other accounting software, you need to understand the basics of startup accounting.

Key Takeaways

- Learn the basics of startup accounting and bookkeeping to familiarize yourself with your record-keeping and tax responsibilities

- Investing in good accounting software for startups will keep you and your business on track throughout the year

- Keep your paperwork organized; you will save time and money in the long run

- Research your options for growing your business—loans and capital are available to start-ups if you know where to look

What this article covers:

- Why Is Accounting Important for a Startup Business?

- What Financial Records Should A Startup Have?

- What Are the Basics of Bookkeeping?

- How Do You Start a New Business Accounting System?

- Accounting Software for Startups

- Conclusion

- Frequently Asked Questions

Why Is Accounting Important for a Startup Business?

Running a business is based on the bottom line. The success of your startup is based on efficient budget management, balancing the books, and modifying financial strategies when needed. Effective accounting practices and sound financial management results in returns for the stakeholders and business owners.

Here are some of the key benefits of accounting for startups:

- An accounting process allows business owners to see where it stands and how it performs financially.

- It allows businesses to understand their financial data, past activity, and where they currently stand to plan for the future.

- Accounting allows startup businesses to keep track of their debts from suppliers and lenders for goods/services purchased and receivables from customers for services rendered or goods sold.

- Small-business and startup owners use financial accounting to communicate information externally to external stakeholders that use a company’s financial information, such as banks, the IRS, suppliers, creditors, potential investors, and leasing companies.

- Accounting is also used to share company strengths and weaknesses with employees.

- Small business owners may use financial accounting information to analyze competitors and evaluate investment opportunities.

What Financial Records Should A Startup Have?

Startups should keep track of all their documents showing transactions and records. So, this means everything. Examples of some financial reporting and records include:

- Bank Statements

- Credit Card Statements

- Bills

- Receipts

- Invoices

- Financial Statements

- Tax Forms

- Tax Returns and Supporting Documents

What Are the Basics of Bookkeeping?

You have so much to think about when starting a business! It can be overwhelming, but learning the basics and deciding how to tackle your financial records early is essential.

Every business owner needs to have a structured method of bookkeeping that records the money coming in and going out of the business. This will help you monitor revenue and expenses, track budgets, fulfill financial obligations, and take action if problems arise.

Bookkeeping is essential! Here are a few accounting basics that will ensure a startup’s financial health:

Analyzing Business Transactions

The bookkeeping process involves keeping track of business transactions and making specific entries. Accounting systems and bookkeeping software like FreshBooks have a chart that lists all your accounts payable and their categories. For example, you can post all sales to income accounts and cash outflows to expense accounts.

Writing Journal Entries

A journal keeps a daily record of all transactions. The journal entries are made from documents that contain financial information, such as receipts, bills, and invoices.

In this accounting method, each transaction is assigned to a specific account using journal entries, and the changes in the accounts are recorded using debits and credits.

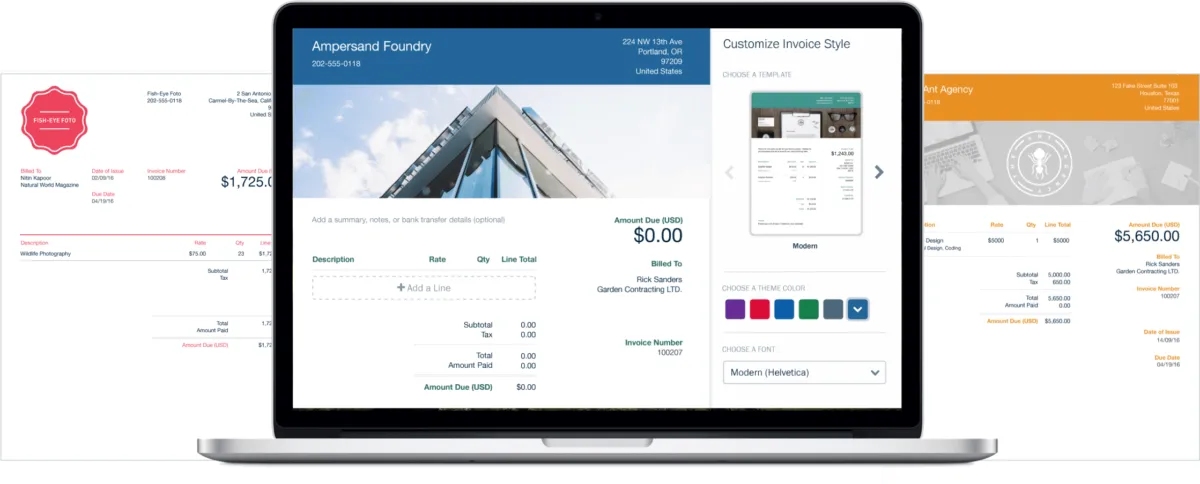

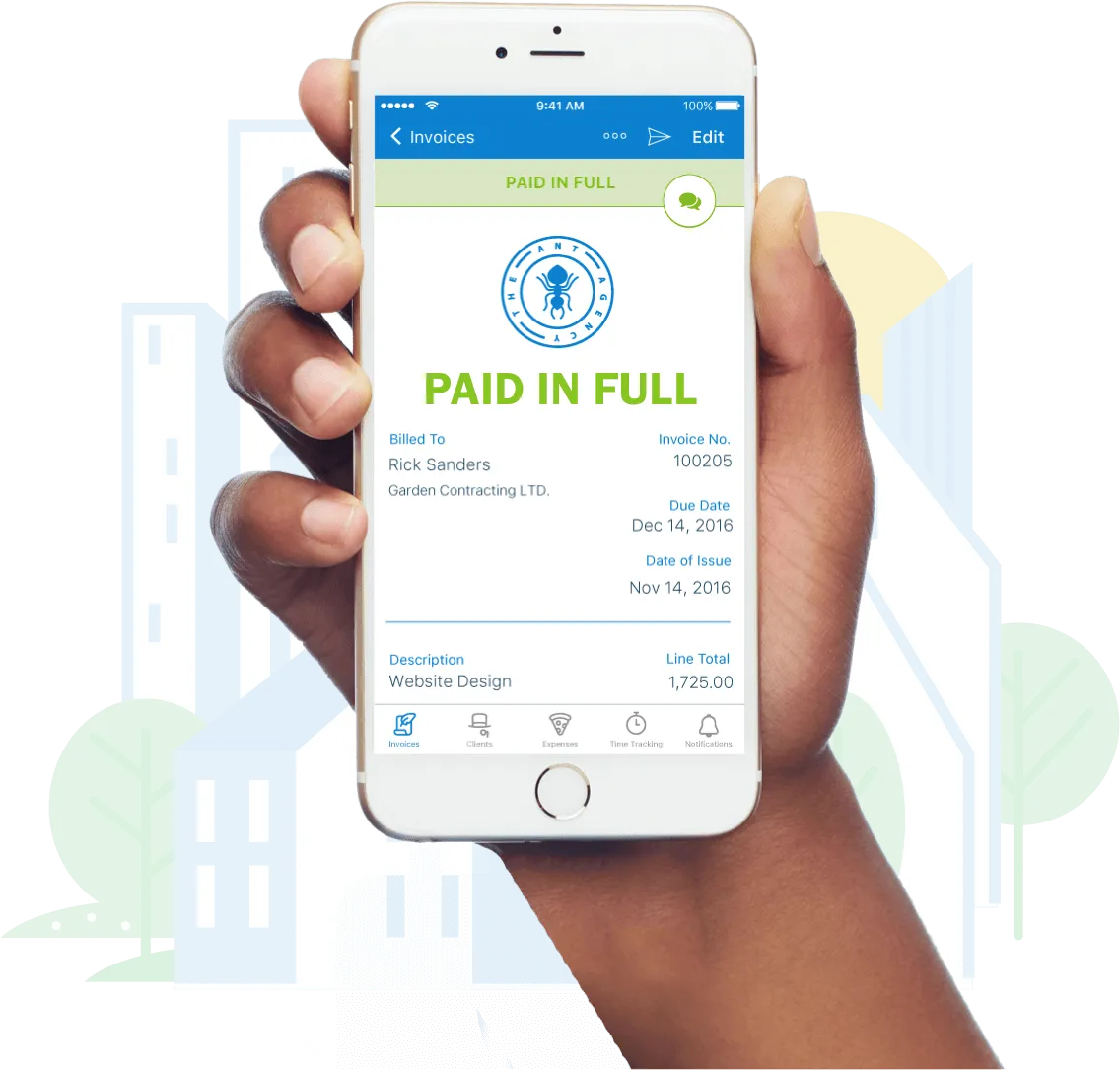

Keeping Invoices

Invoices are documents that list products and services businesses provide to their clients. The client has an obligation to pay the business for services rendered or goods sold. In short, invoices are an important part of how small businesses make money. If you’ve just started your own business, you might want to use an invoice template for keeping track. As you go forward and grow, Freshbooks has excellent invoice software that will allow you to automate and simplify the invoice process. This will save you time and money and get you paid faster. Click here to try it for free today.

Posting to Ledger Accounts

A collection of related accounts is known as a ledger. The accounts are generally categorized into the 5 main account types: assets, liabilities, equity, revenues, and expenses. When a journal entry shows a change, the balances are updated in the appropriate accounts. The information in the journal that appears in order is summarized in the ledger on an account-by-account basis. To simplify the process, you can use our free general ledger template that helps you organize and track financial data efficiently. For an in-depth understanding of ledgers, consider reading our article on What is a Ledger. It covers key topics like The Difference Between Journals and Ledgers and How to Write an Accounting Ledger.

The information in the journal that appears in order is summarized in the ledger on an account-by-account basis.

Trial Balances

To ensure that journal entries have been recorded and posted correctly, small businesses use the trial balance accounting method to double-check account balances for a given time period. A trial balance ensures that the debit and credit balances in the ledger accounts match. If they don’t, you know an error has been made.

Reconciling Bank Statements

A bookkeeper reconciles bank statements regularly to ensure your bank account balance matches the cash balance in your ledger. This can be done weekly, monthly, or even quarterly. If the amounts in the bank statement and internal records don’t match, you’ll need to find out where the discrepancies are and adjust the entries to ensure they match the bank statements correctly. An accounting system like FreshBooks can be helpful.

Adjusting entries are generally unrecorded transactions that have yet to occur but will occur at the end of the reporting period to record unrecognized revenue or expenses or to correct any recorded transactions.

Tax Returns

There’s no question that keeping records of your business’s tax returns is essential. What’s also imperative is keeping track of and maintaining these records and forms throughout the year. Whether it’s your first business tax return or you’re a pro, having an organized system for your documents will save you a lot of stress. FreshBooks can help by keeping your accounting systems organized, allowing you and your tax professional to find all the information when you need to file.

Closing Accounts

Most businesses have revenue and expense bank accounts (AKA temporary accounts) that provide information for the company’s income statement. At the end of the accounting cycle, these accounts are closed, which means the balance of the temporary accounts is reduced to zero.

A report called Profit and Loss is created to show a business entity’s net income or loss in that particular accounting period.

Good bookkeeping provides entrepreneurs and small business owners with detailed, accurate, timely records that assist decision-making, taxes, and audits. It’s an essential part of good business management and business growth.

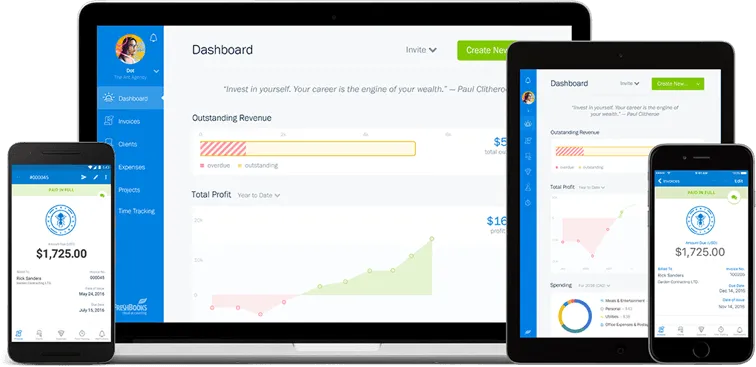

Accounting Software for Startups

Accounting software is one of the most helpful and powerful tools you can add to your startup accounting toolbelt. With self employed accounting software, you can track business transactions, create invoices, maintain financial records, and be ready for your tax returns. This type of software will inform you about your company’s financial position and make it easy to keep files, receipts, documents, and records in order.

Popular Accounting Software for Startups

There are many different accounting software products available to small businesses. The top software options you may wish to choose from to manage to account for your business include:

FreshBooks

FreshBooks accounting software for startups is the top choice for the startup owner who wants to make life easier for themselves. FreshBooks is an all-in-one startup accounting software solution that handles your bookkeeping needs and provides important insights into your finances as your business grows. Click here to try it for free today.

QuickBooks Online

Quickbooks Online is another popular online accounting software providing users with the services they need to maintain a financially healthy business.

Xero

Xero is another emerging online accounting software company providing practical tools and bank connections with a variety of plans to suit any size of business.

How Do You Start a New Business Accounting System?

Business owners can follow this checklist to get started:

- Open a separate bank account to separate your business finances from personal accounts.

- Track your business expenses regularly, including receipts, bills, invoices, and proof of payments, ensuring they are reflected on financial statements and tax returns.

- Based on your business structure and accounting needs, establish a bookkeeping system. You can do this independently, outsource it, or hire an in-house bookkeeper. Understand your tax obligations; ensure you adhere to filing deadlines and are aware of any penalties involved.

- Use the balance sheet, cash flow statement, profit and loss report, and other financial reports and documents to evaluate your business’s financial health regularly.

As your startup grows and makes more revenue, your recordkeeping system will become more complex and crucial to maintain. This is why starting with a well-organized system as you run your business is essential. You can use simple and intuitive accounting software for startups to automate the accounting process and get an up-to-date view of your cash flow. One of your best choices is to try FreshBooks accounting software for free. It can help you navigate the growth of your business and keep your startup’s financial health in tip-top shape. Click here to try it for free today.

How do you get loans and funding for your startup?

- The Founder’s Guide to Startup Funding: Get loads of information and options to get the business loan or financing you need to get your business off the ground and grow.

- Using Student Loans to Start a Business: Is It Worth the Risk?: Here, you’ll find all the pros and cons of using student loans to start a business.

- Starting a Business With Student Loan Debt: Is It Possible?: Hot tip, it is possible, but there are a few things you need to know, find out here.

Conclusion

As you probably already know, starting a new business is a lot of work! One of the most important steps you need to take to set up your accounting system is to make sure that your files and documents are organized. If you familiarize yourself with basic accounting terms and invest in a good accounting software package, you’ll be well on your way to success.

Record-keeping and accounting don’t have to be scary. If you need an easy-to-understand accounting software package with great customer service and tech support, FreshBooks can help.

FAQs on Accounting for Startups

Do startups need accountants?

If your business is small, you might choose to handle the accounting yourself rather than hiring an accountant, and only seek professional when it’s time to prepare taxes. But regular sound professional advice is invaluable and can make your business successful.

Do startups use GAAP?

Smart startups definitely use GAAP! These are the Generally Accepted Accounting Principles that are used to standardize accounting practice across the US. GAAP helps provide clear information on your business’s financial health.

How much do startups spend on accounting?

That really depends on the startup. It’s wise to hire a person or invest in a system to help manage the accounting in your business. Look at your needs, and don’t neglect to learn the basics. FreshBooks can help with resources for small businesses and free trials of software.

What are the five basic accounts in bookkeeping?

The five most basic accounts in bookkeeping are Assets, Liabilities, Equity, Revenue, and Expenses. Most business accounts and cash accounting activities can be categorized into one of these areas. If you want to learn more about bookkeeping, follow our guide on starting how to become a bookkeeper.

Where do startup costs go on a balance sheet?

A variety of expenditures can be involved in establishing a business; obtaining equipment or stock, market research, and even staff training can qualify as start-up costs. Startup costs for a new business are categorized as income and listed in a balance sheet’s Equity section.

How can startups save money on accounting?

Startups can save money on accounting immediately by taking meticulous care of their records, receipts, and spending. Choosing an accounting program that can help you organize everything in one place is invaluable.

Reviewed by

Kristen Slavin is a CPA with 16 years of experience, specializing in accounting, bookkeeping, and tax services for small businesses. A member of the CPA Association of BC, she also holds a Master’s Degree in Business Administration from Simon Fraser University. In her spare time, Kristen enjoys camping, hiking, and road tripping with her husband and two children. In 2022 Kristen founded K10 Accounting. The firm offers bookkeeping and accounting services for business and personal needs, as well as ERP consulting and audit assistance.

RELATED ARTICLES

How do you use the Shareholders Equity Formula to Calculate Shareholders’ Equity for a Balance Sheet?

How do you use the Shareholders Equity Formula to Calculate Shareholders’ Equity for a Balance Sheet? How Do You Calculate Operating Income?

How Do You Calculate Operating Income? Operating Income vs. Net Income: Which Should You Pay Attention To?

Operating Income vs. Net Income: Which Should You Pay Attention To? How to Calculate Goodwill of a Business: Step-By-Step

How to Calculate Goodwill of a Business: Step-By-Step What Are Operating Activities in a Business?

What Are Operating Activities in a Business? Foreign Currency Translation: International Accounting Basics

Foreign Currency Translation: International Accounting Basics